According to the August 14th USDA Cotton and Wool Outlook, global cotton production in 2020/21 is projected at 116.2 million bales, 5.5% (6.7 million bales) below the previous year and the smallest crop in 4 years.

In 2020/21, cotton production expectations for most major-producing countries are for smaller crops, with Pakistan and Australia notable exceptions. The global cotton harvested area is forecast at 33.0 million hectares (81.5 million acres), nearly 6% below 2019/20’s 35.0 million hectares (86.5 million acres), which was the highest since 2011/12. Area declines are generally attributable to lower cotton prices, which resulted from stock levels rising significantly in 2019/20. The 2020/21 global cotton yield is forecast at 768 kg/hectare (685 lb./acre), marginally above the 2019/20 yield.

World cotton production remains concentrated among a few countries. In 2020/21, the top four cotton-producing countries are forecast to account for 73% of total production, slightly below 2019/20 but similar to the 2018/19-2019/20 average. India is forecast to remain the leading producer in 2020/21, accounting for 24.5% of the global crop projection. China is expected to contribute 23% of the total, while the U.S. and Brazil are projected to account for 15% and 10%, respectively, of the world cotton crop in 2020/21.

India is projected to produce 28.5 million bales of cotton in 2020/21, 2 million bales below the previous year, as a 6% reduction in area to 12.5 million hectares combined with a slightly lower yield expectation of 496 kg/hectare. For China, 2020/21 cotton production is forecast at 26.5 million bales, nearly 3% (750,000 bales) below 2019/20. Cotton production is concentrated in the high-yielding Xinjiang region, contributing heavily to the 2020/21 national yield projected at 1,748 kg/hectare; however, the second highest yield on record is more than offset by lower area, forecast at 3.3 million hectares, leading to the crop decline.

Cotton production in Brazil is forecast at 12.0 million bales in 2020/21, 1.2 million bales (9%) lower than the 2019/20 record crop. Rising stocks are expected to reduce Brazil’s upcoming cotton area for 2020/21, where planting will largely occur in January. Brazil’s yield is currently forecast at 1,686 kg/hectare, 2% below 2019/20. In contrast, cotton production in Pakistan and Australia is projected to increase in 2020/21. For Pakistan, the crop is forecast at 6.5 million bales (up 300,000 bales), as a rebound in yield to 590 kg/hectare offsets a slightly lower area in 2020/21. For Australia, both area and production are forecast to rebound dramatically from the drought-reduced crop of 2019/20. Area is forecast at 180,000 hectares, while production is forecast at 1.7 million bales, nearly 1.1 million bales higher.

Global Cotton Mill Use, Trade and Stocks Higher in 2020/21

Estimates for world cotton mill use are lowered in July for both 2020/21 and 2019/20, as the global economic slowdown related to the COVID-19 pandemic continues to weigh on consumer demand for apparel items, including cotton products.

Despite the reductions, global cotton consumption for 2020/21 is forecast at 114.3 million bales, or about 12% above the revised 2019/20 estimate of 102.4 million bales, which is 15% below 2018/19.

For 2020/21, mill use for all major countries is forecast to experience a rebound as each country’s cotton spinning industry adapts to the anticipated recovery of the global economy. Adequate and relatively inexpensive cotton supplies will help the resurgence, which is expected to be led by China and India. China is forecast to account for 32% (37 million bales) of global cotton mill use in 2020/21, while India contributes an additional 20% (23 million bales). In addition, Pakistan is expected to account for 9% (10.3 million bales), while Bangladesh, Turkey and Vietnam each contribute 6%.

Global cotton trade in 2020/21 is forecast at 41.8 million bales, about 4.5% above 2019/20. With total trade up 1.8 million bales, exports from several countries are expected to rise in 2020/21. Shipments from Brazil and India are likely to increase as supplies there have grown considerably in recent years. Brazil’s cotton exports for 2020/21 are forecast at 9.0 million bales, 3% above the year before. For India, exports are projected to reach 4.5 million bales, an increase of 1.5 million bales. Meanwhile, exports from the U.S. and Australia are forecast slightly lower in 2020/21.

Higher cotton import projections are forecast for most of the leading importing countries for 2020/21. China, the leading importer, is expected to import 9.0 million bales of raw cotton, 24% above 2019/20; China imported 9.6 million bales in 2018/19. For Bangladesh and Vietnam, 2020/21 imports are projected at 7.1 million bales (up 6%) and 7.0 million bales (up 8%), respectively. Pakistan’s cotton imports are also forecast higher at 3.9 million bales.

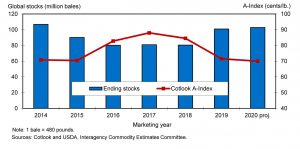

World cotton ending stocks are forecast at 102.8 million bales in 2020/21, nearly 1.9 million bales above 2019/20, as global production is projected to exceed mill use for the second consecutive year. Despite stocks reaching the highest level in 6 years, the 2020/21 stocks-to-use ratio is forecast to decrease from 2019/20’s 99% to 90%. However, world cotton stocks outside of China are expected to be higher in 2020/21, pressuring prices. Consequently, the average world cotton price (A Index) in 2020/21 is expected to decline slightly from the 2019/20 estimate of 71.5 cent/lb.